For years, several homeowners were prevented from moving up because of negative equity which means that they owe more than what the house is worth. They were locked-in to their location because of their low home values. Now that the economy is improving and their home market value has increased, they don't want to move because of the rock bottom rate they have when they bought or refinanced last couple of years. In late 2012, the interest rate was 3.3%. Now that the interest rate is starting to head back up, they are hesitant to move.

John Moony, managing vice president of Guaranteed Rate, a national mortgage company based in the Chicago area, says that even a 1 percent increase in mortgage rates can make a big difference in a home owner’s decision-making process. He says a 1 percent increase in interest rates generally equates to a 10 percent reduction in purchasing power. In practical terms, that means a family looking to keep their mortgage payment below, say, $1,500 a month will need to lower the maximum price they can pay for a house from $300,000 to $270,000 if interest rates go up one percentage point.

John Moony, managing vice president of Guaranteed Rate, a national mortgage company based in the Chicago area, says that even a 1 percent increase in mortgage rates can make a big difference in a home owner’s decision-making process. He says a 1 percent increase in interest rates generally equates to a 10 percent reduction in purchasing power. In practical terms, that means a family looking to keep their mortgage payment below, say, $1,500 a month will need to lower the maximum price they can pay for a house from $300,000 to $270,000 if interest rates go up one percentage point.

Thursday, July 31, 2014

Tuesday, July 29, 2014

Pending Home Sales Ease Slightly But Still Above Average

After climbing for three straight months, pending home sales dipped slightly in June, held back by inventory shortages in some markets, tight credit and stagnant wages, the National Association of Realtors said today.

NAR’s pending home sales index, a forward-looking indicator that tracks contract signings that usually result in home sales, slipped 1.1 percent from May to June, and was down 7.3 percent from the same time a year ago.

Despite June’s decrease, the pending home sales index remained above 100, an “average” level of contract activity, for the second consecutive month.

NAR Chief Economist Lawrence Yun said he expects sales of existing homes to edge up during the second half of the year, but that sales for the year as a whole will be down 2.8 percent from 2013, a projection that aligns with Fannie Mae’s latest forecast.

Yun said cooling price appreciation and expanding inventory should drive the improvement.

“The good news is that price appreciation has decreased to its slowest pace since March 2012 behind much-needed increases in inventory,” Yun said in a statement. “With rents rising 4 percent annually, potential buyers are less likely to experience sticker shock and can make smart decisions on whether or not it makes sense to buy or continue renting.”

Yun expects that the national median existing-home price should grow between 5 and 6 percent this year and in 2015.

Written by: Teke Wiggin, Staff writer of Inman News

Friday, July 25, 2014

July/August 2014 - MARKET PULSE

Mortgage rates remain low but are poised to rise, which would dampen

affordability and therefore demand. Even so, both closed sales and

contract signings show signs of a turnaround after months of steady

declines.

From Realtor Mag

From Realtor Mag

Thursday, July 24, 2014

Mortgage Rates Remain Near Year's Low

MCLEAN, VA--(Marketwired - Jul 24, 2014) - Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing average fixed mortgage rates largely flat for the week, remaining just above their lows for 2014 and helping to support homebuyer affordability.

News Facts

#MortgageRates

Written by Freddie Mac and published in FreddieMac.com

- 30-year fixed-rate mortgage (FRM) averaged 4.13 percent with an average 0.6 point for the week ending July 24, 2014, unchanged from last week. A year ago at this time, the 30-year FRM averaged 4.31 percent.

- 15-year FRM this week averaged 3.26 percent with an average 0.6 point, up from last week when it averaged 3.23 percent. A year ago at this time, the 15-year FRM averaged 3.39 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.99 percent this week with an average 0.5 point, up from last week when it averaged 2.97 percent. A year ago, the 5-year ARM averaged 3.16 percent.

- 1-year Treasury-indexed ARM averaged 2.39 percent this week with an average 0.4 point, unchanged from last week. At this time last year, the 1-year ARM averaged 2.65 percent.

#MortgageRates

Written by Freddie Mac and published in FreddieMac.com

Wednesday, July 23, 2014

3 Things Never to Say to a Creditor

This is a video created by Corey Goldstein to share with people who are working to improve their credit standing. Watch the video below:

What are Mortgage Points?

The structure of home mortgages varies around the world. Paying for mortgage points is a common practice in the United States. There are 2 kinds of mortgage points that I know of. They are:

- Origination Point - According to Investopedia.com, origination point is a type of fee borrowers pay to lenders or loan officers in order to compensate them for the role they play in evaluating, processing and approving mortgage loans. Credit history is one factor that plays a role in the amount of origination points a borrower needs to pay. It is usually 1% of the total amount mortgaged. Not all mortgage providers require the payment of origination points.

- Discount Point - According to Investopedia.com, discount point is a type of prepaid interest mortgage borrowers can purchase that lowers the amount of interest they will have to pay on subsequent payments. Each discount point generally costs 1% of the total loan amount and depending on the borrower, each point lowers your interest rate by one-eighth to one one-quarter of your interest rate.

Should You Pay For Points?

The decision of whether or not to pay for points generally focuses on discount points, and requires being able to understand the mortgage payment structure. There are two primary factors to weigh when considering whether or not to pay for discount points. The first involves the length of time that you expect to live in the house. In general, the longer you plan to stay, the bigger your savings if you purchase discount points.Friday, July 18, 2014

Buyers on the Fence????

We have often broken down the opportunity that exists now

for Millennials who are willing and able to purchase a home NOW... Here

are a couple other ways to look at the cost of waiting.

Let’s say you're 30 and your dream house costs $250,000 today, at 4.41% your monthly Mortgage Payment with Interest would be $1,253.38.

But you’re busy, you like your apartment, moving is such a

hassle...You decide to wait till the end of next year to buy and all of a

sudden, you’re 31, that same house is $270,000, at 5.7%. Your new payment per month is $1,567.08.

The difference in payment is $313.70 PER MONTH!

That’s like taking a $10 bill and tossing it out the window EVERY DAY!

Or you could look at it this way:

- That’s your morning coffee everyday on the way to work (Average $2) with $12 left for lunch!

- There goes Friday Sushi Night! ($80 x 4)

- Stressed Out? How about 3 deep tissue massages with tip!

- Need a new car? You could get a brand new $22,000 car for $313.00 per month.

Let’s look at that number annually! Over the course of your new mortgage at 5.7%, your annual additional cost would be $3,764.40!

Had your eye on a vacation in the Caribbean? How about a 2-week trip

through Europe? Or maybe your new house could really use a deck for

entertaining. We could come up with 100’s of ways to spend $3,764, and

we’re sure you could too!

Over the course of your 30 year loan, now at age 61, hopefully you are ready to retire soon, you would have spent an additional $112,932, all because when you were 30 you thought moving in 2014 was such a hassle or loved your apartment too much to leave yet.

Or maybe there wasn’t an agent out there who educated you on the true

cost of waiting a year. Maybe they thought you wouldn’t be ready, but

if they showed you that you could save $112,932, you’d at least listen to what they had to say.

They say hindsight is 20/20, we’d like to think that 30 years from now when you are 60, looking back, you would say to buy now…

kcm 2014

Thursday, July 17, 2014

Does a Homeowner Gets Notice of a Trustee Sale?

Foreclosure by judicial sale, more commonly known as judicial foreclosure, which is available in every state (and required in many), involves the sale of the mortgaged property under the supervision of a court, with the proceeds going first to satisfy the mortgage; then other lien holders; and, finally, the mortgagor/borrower if any proceeds are left. Under this system, the lender initiates foreclosure by filing a lawsuit against the borrower. As with all other legal actions, all parties must be notified of the foreclosure, but notification requirements vary significantly from state to state. A judicial decision is announced after the exchange of pleadings at a (usually short) hearing in a state or local court. In some rather rare instances, foreclosures are filed in federal courts.

Foreclosure by power of sale, also known as nonjudicial foreclosure, is authorized by many states if a power of sale clause is included in the mortgage or if a deed of trust with such a clause was used, instead of an actual mortgage. In some states, like California, nearly all so-called mortgages are actually deeds of trust. This process involves the sale of the property by the mortgage holder without court supervision (as elaborated upon below). This process is generally much faster and cheaper than foreclosure by judicial sale. As in judicial sale, the mortgage holder and other lien holders are respectively first and second claimants to the proceeds from the sale.

In Arizona, adopted the non-judicial foreclosure where a deed of trust, not a mortgage, is generally the document used for a security interest in real property. A deed of trust can be foreclosed by a trustee's sale without any court action. The only requirement for notice to the homeowner of a trustee's sale is mailing the recorded notice of trustee's sale by certified or registered mail to the borrower's address on the deed of trust, or to the borrower's last known address.

Foreclosure by power of sale, also known as nonjudicial foreclosure, is authorized by many states if a power of sale clause is included in the mortgage or if a deed of trust with such a clause was used, instead of an actual mortgage. In some states, like California, nearly all so-called mortgages are actually deeds of trust. This process involves the sale of the property by the mortgage holder without court supervision (as elaborated upon below). This process is generally much faster and cheaper than foreclosure by judicial sale. As in judicial sale, the mortgage holder and other lien holders are respectively first and second claimants to the proceeds from the sale.

In Arizona, adopted the non-judicial foreclosure where a deed of trust, not a mortgage, is generally the document used for a security interest in real property. A deed of trust can be foreclosed by a trustee's sale without any court action. The only requirement for notice to the homeowner of a trustee's sale is mailing the recorded notice of trustee's sale by certified or registered mail to the borrower's address on the deed of trust, or to the borrower's last known address.

Wednesday, July 16, 2014

9 WAYS BECOMING A HOMEOWNER CAN CHANGE YOUR LIFE

Homeownership. It shifts so many things. If you're coming from an apartment, you may experience conveniences like direct-access garages and walls that aren't shared for the first time. If you've been renting a home, you will probably feel a new sense of security and peace of mind once the mortgage is in our name. Not to mention the itch to repaint, re-imagine, and redo at least a few dozen things.

Want to know just how becoming a homeowner can change your life? Read on.

1. Financial Security

"The largest measurable financial benefit to homeownership is price appreciation," said Investopedia. "Price appreciation helps build home equity." Added Real Estate ABC: "The principle you pay on the mortgage is like putting money in the bank, in the form of equity."

2. Peace of mind

If you worry every time your lease comes up for renewal, those days are gladly over. Unless you refinance or take cash out once you have enough equity, your house payment is your house payment.

3. Pride of ownership

The feeling you get when you come home to your place - the place you scrimped and saved for and the place that represents a lifelong dream - well, there's just no substitute.

4. Stake in your neighborhood

Pride of ownership extends to the homes and area around your house as well. Whether or not you move to a neighborhood with a homeowner's association, buying a house will undoubtedly make you more invested in what's going on around you. And that can mean increased property values if neighbors band together for common improvements.

5. Increased interest in HGTV. And DIY channel. And weekends at Home Depot.

Don't be surprised if you start quoting Drew and Jonathan Scott or using terms like "mitered corners" and "refaced cabinets." Which is good news, because the changes you make to your home won't just mean greater enjoyment while you live there, but also potentially greater profit when you go to sell.

"Home ownership means you have free rein in the aesthetics of the home. When renting, you do not have the advantage of changing your environment to please you," said Real Estate ABC. "You may be able to paint a room, but need to repaint back to the original color scheme when you move. Owning your own home means you can do whatever you please to make your environment both personalized and, in the process, add value to the home."

6. Your honey do list may increase

But so will your satisfaction.

7. Tax breaks

"The second largest financial benefit of owning a home is tax savings," said Investopedia. "The biggest of these is the ability to deduct the annual interest paid on a mortgage from income. Private mortgage insurance may also be a write off, on addition to fees paid at closing. If you have paid points, either discount or origination, you can deduct these as well."

8. Expert knowledge of interest rates, neighborhood home prices, and area sales trends

When you're in the process of buying and after you close escrow, you're more likely to be tuned into what's going on in the market and in your neighborhood. This can help you to make smart decisions about updates, upgrades, and refinancing, and can also make you a trusted resource among your friends who want to buy.

9. More financial responsibility in other parts of your life

With a home to take care of, you may be more clued in to other long-term investments and less wiling to spend frivolously.

Tuesday, July 15, 2014

Rich Chinese are Buying America's Real Estate

The US Housing recovery is still going on with the Chinese leading the pack of international buyers. Chinese buying was up 70% - nearly 1 in 4 dollars of all foreign purchases according to National Association of Realtors.

Canadians are number 1 in terms of total homes bought but the Chinese buy more expensive homes with an average price of $591,000.00. The Chinese also brought more cash to the table with more than three-fourth of their purchases were cash transaction.

California is the biggest market for the Chinese followed by Washington State, New York, Pennsylvania, and then Texas. 39% of the Chinese buyers said that they will use it as their main home. Others are buying condos for their children attending US Colleges and Universities to save on dormitory fees and benefit from the home appreciation by the time their student graduate. Others are buying cheap homes and renting them out. Still others use them as vacation homes for a couple of weeks a year and then rent them out for the rest of the time.

From Les Christie @CNNMoney

Canadians are number 1 in terms of total homes bought but the Chinese buy more expensive homes with an average price of $591,000.00. The Chinese also brought more cash to the table with more than three-fourth of their purchases were cash transaction.

California is the biggest market for the Chinese followed by Washington State, New York, Pennsylvania, and then Texas. 39% of the Chinese buyers said that they will use it as their main home. Others are buying condos for their children attending US Colleges and Universities to save on dormitory fees and benefit from the home appreciation by the time their student graduate. Others are buying cheap homes and renting them out. Still others use them as vacation homes for a couple of weeks a year and then rent them out for the rest of the time.

From Les Christie @CNNMoney

Monday, July 14, 2014

Buy or Rent?

BUY or RENT? This is a question that homebuyers always asked. It is not a question that is easy to answer. It all depends on the readiness of the individual to commit to taking on a mortgage, taking care of a house and availability of the right home.

There is another way of understanding the financial impact of buying vs renting. There is a tool that can be used to determine the net cost of buying a home vs the cost of renting over time.

Please click here to compare your costs of buying and renting. Click "Advanced options" to change inputs like down payment, mortgage rate, income tax rate, and inflation rate.

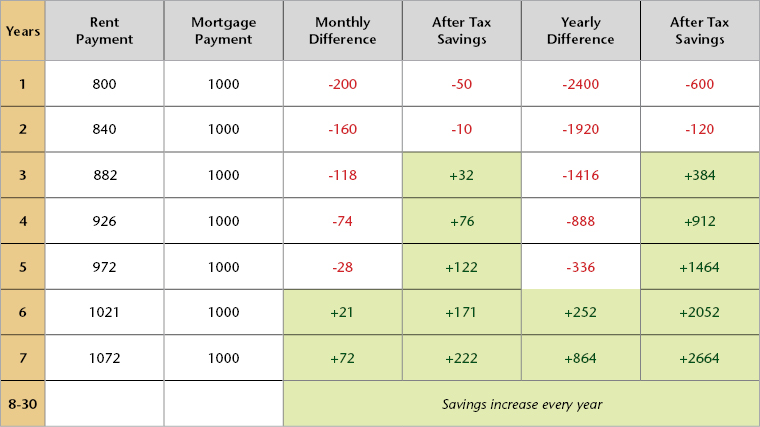

Buy vs. Rent Comparison as published by The National Association of Realtors.

The chart below shows a cost comparison for a renter and a homeowner over a seven year period. The renter starts out paying $800 per month with annual increases of 5% The homeowner purchases a home for $110,000 and pays a monthly mortgage of $1,000 After 6 years, the homeowner's payment is lower than the renter's monthly payment With the tax savings of homeownership, the homeowner's payment is less than the rental payment after 3 years.

There is another way of understanding the financial impact of buying vs renting. There is a tool that can be used to determine the net cost of buying a home vs the cost of renting over time.

Please click here to compare your costs of buying and renting. Click "Advanced options" to change inputs like down payment, mortgage rate, income tax rate, and inflation rate.

Friday, July 11, 2014

How Lenders Offer Zero Points or Lower Mortgage Rates

A lender may get daily rate sheets from

their secondary marketing department or from wholesale mortgage lenders.

These mortgage interest rates are usually not for public view, because

they show the price of a home loan before the retail mark-up.

On the rate sheet, incremental mortgage rates correspond to the cost of the rate expressed in terms of “basis points”. One point is equal to one percent of the loan amount.

The rates with numbers in parenthesis next to them indicate “rebate” points paid to the lender for selling a loan at a premium. The rates without numbers in parenthesis show the lender’s “cost” to sell a loan at that particular interest rate. The rate with corresponding zeros is the “par” price, which means the lender incurs no cost and they receive no rebate points for that mortgage interest rate.

Lower mortgage rates have a higher up-front cost because the mortgage holder earns less interest over the term of the loan. Conversely, higher rates have lower short term costs because the mortgage holder will earn more in interest over the life of the loan, rather than points paid up-front.

In order to quote mortgage interest rates,a loan officer or broker adds points to the wholesale rate sheet pricing, which is essentially a commission. The lender normally sets a policy on the minimum and maximum points the loan officer adds to the rate cost. This pricing structure provides flexibility to offer lower mortgage rates with higher points, or a zero point mortgage at a higher rate.

Current rates on a lender's website have already been adjusted to show a retail price.

Written by Rick Smith of MyRealtyTimes

On the rate sheet, incremental mortgage rates correspond to the cost of the rate expressed in terms of “basis points”. One point is equal to one percent of the loan amount.

The rates with numbers in parenthesis next to them indicate “rebate” points paid to the lender for selling a loan at a premium. The rates without numbers in parenthesis show the lender’s “cost” to sell a loan at that particular interest rate. The rate with corresponding zeros is the “par” price, which means the lender incurs no cost and they receive no rebate points for that mortgage interest rate.

Lower mortgage rates have a higher up-front cost because the mortgage holder earns less interest over the term of the loan. Conversely, higher rates have lower short term costs because the mortgage holder will earn more in interest over the life of the loan, rather than points paid up-front.

In order to quote mortgage interest rates,a loan officer or broker adds points to the wholesale rate sheet pricing, which is essentially a commission. The lender normally sets a policy on the minimum and maximum points the loan officer adds to the rate cost. This pricing structure provides flexibility to offer lower mortgage rates with higher points, or a zero point mortgage at a higher rate.

Current rates on a lender's website have already been adjusted to show a retail price.

Written by Rick Smith of MyRealtyTimes

Thursday, July 10, 2014

Top Amenities Buyers Will Make Sacrifices For

Home buyers are showing some willingness to pay more for certain amenities in a home, according to the latest PulteGroup Home Index Survey of more than 1,000 adults ages 25 to 65.

What's surprising is that buyers say they'd give up some pretty alluring draws about a property for certain amenities: Forty-four percent surveyed say they're willing to give up a location near public transportation in exchange for certain amenities, and 35 percent say they'd give up better schools and proximity to entertainment and shopping.

So what are these amenities that home buyers want so badly? Fifty-one percent surveyed say they want their next home to be larger than their current residence, and 64 percent say they prefer a move-in ready home.

Among the most important features home buyers identified:

"His and her closets" in the master bedroom (31%) and spa-like master bathrooms (23%)

A large eat-in kitchen area (23%) and a kitchen island (22%)

At least one bathtub in a home (54%)

"In addition to the more common home options, we're starting to see regional trends emerging among home buyer preferences," says Ryan Marshall , PulteGroup Inc.'s executive vice president of homebuilding operations, marketing and sales. "From outdoor kitchens in Florida, to spice kitchens in California, shoppers are increasingly discerning when it comes to home features that could be the deciding factor in their next move." Folding, accordion-style glass doors are popular in the Southwest, while multi-generation floor plans and screened-in porches are popular in the Southeast, according to the survey. In the Northeast, balconies off the kitchen and rooftop terraces are sought-after, while "Jack 'n' Jill" bedrooms are in high demand in the Midwest. The most important areas to home buyers when choosing a new home: kitchen (29%), bedroom (22%), and living room (18%). "Consumers today aren't just looking for the biggest house on the block. They're looking for more efficient use of space and a greater area allocated to 'workhorse' spaces, like the kitchen," says Marshall. "Home buyers want unique features and amenities and will do what it takes to find the home they truly want, even if they have to pay more for a move-in ready home."

DAILY REAL ESTATE NEWS | THURSDAY, JULY 10, 2014 From Realtor.Com

Source: PulteGroup Home Index

What's surprising is that buyers say they'd give up some pretty alluring draws about a property for certain amenities: Forty-four percent surveyed say they're willing to give up a location near public transportation in exchange for certain amenities, and 35 percent say they'd give up better schools and proximity to entertainment and shopping.

So what are these amenities that home buyers want so badly? Fifty-one percent surveyed say they want their next home to be larger than their current residence, and 64 percent say they prefer a move-in ready home.

Among the most important features home buyers identified:

"In addition to the more common home options, we're starting to see regional trends emerging among home buyer preferences," says Ryan Marshall , PulteGroup Inc.'s executive vice president of homebuilding operations, marketing and sales. "From outdoor kitchens in Florida, to spice kitchens in California, shoppers are increasingly discerning when it comes to home features that could be the deciding factor in their next move." Folding, accordion-style glass doors are popular in the Southwest, while multi-generation floor plans and screened-in porches are popular in the Southeast, according to the survey. In the Northeast, balconies off the kitchen and rooftop terraces are sought-after, while "Jack 'n' Jill" bedrooms are in high demand in the Midwest. The most important areas to home buyers when choosing a new home: kitchen (29%), bedroom (22%), and living room (18%). "Consumers today aren't just looking for the biggest house on the block. They're looking for more efficient use of space and a greater area allocated to 'workhorse' spaces, like the kitchen," says Marshall. "Home buyers want unique features and amenities and will do what it takes to find the home they truly want, even if they have to pay more for a move-in ready home."

DAILY REAL ESTATE NEWS | THURSDAY, JULY 10, 2014 From Realtor.Com

Source: PulteGroup Home Index

Wednesday, July 9, 2014

A Strong Recovering Market

In 2012, after overshooting on the downside, Phoenix’s housing prices rebounded strongly and the metro was fast on the mend. During this time, Phoenix attracted foreign and large US investor interest and quickly worked through its foreclosure inventory, turning many into rentals for the recently displaced foreclosure victims. This triggered historically high rental yields and generally inspired confidence in the housing market’s trajectory at the time.

Today, the frenzy in Phoenix has subsided but housing appreciation is still positive, just returning to long term fundamentals and a more sustainable, long-term growth trajectory. Employment rates are even, jobs are growing and single-family home prices and listing prices are all rising proportionately. Most importantly, the foreclosure sales that dominated this market during the housing crisis have been cleared allowing Phoenix to recover a great amount of what was lost.

In Phoenix, demand remains high and market fundamentals are strong. A healthy 5.99 Months of Remaining Inventory supports this, as do prices for active listings and sales, which are respectively up by 27 percent and 15 percent from a year ago. Phoenix has returned to a more stable and healthy housing market with a positive five-year forecast.

From PROTECK Valuation Services - Providing insights into the current U.S. housing market and commentary on future trends

Today, the frenzy in Phoenix has subsided but housing appreciation is still positive, just returning to long term fundamentals and a more sustainable, long-term growth trajectory. Employment rates are even, jobs are growing and single-family home prices and listing prices are all rising proportionately. Most importantly, the foreclosure sales that dominated this market during the housing crisis have been cleared allowing Phoenix to recover a great amount of what was lost.

In Phoenix, demand remains high and market fundamentals are strong. A healthy 5.99 Months of Remaining Inventory supports this, as do prices for active listings and sales, which are respectively up by 27 percent and 15 percent from a year ago. Phoenix has returned to a more stable and healthy housing market with a positive five-year forecast.

From PROTECK Valuation Services - Providing insights into the current U.S. housing market and commentary on future trends

Tuesday, July 8, 2014

Existing Home Sales Report

The most important data point revealed in the report was not sales but instead the inventory of homes on the market (supply). The report explained:

Total housing inventory climbed 2.2% to 2.28 million homes available for sale

That represents a 5.6-month supply at the current sales pace.

Unsold inventory is 6.0% higher than a year ago

There were two more interesting comments in the report made by Lawrence Yun, NAR’s chief economist,

“Rising inventory bodes well for slower price growth and greater affordability, but the amount of homes for sale is still modestly below a balanced market.” In real estate, there is a guideline that often applies. When there is less than 6 months inventory available, we are in a sellers’ market and we will see appreciation. Between 6-7 months is a neutral market where prices will increase at the rate of inflation. More than 7 months inventory means we are in a buyers’ market and should expect depreciation in home values. As Yun notes, we are currently in a sellers’ market (prices still increasing) but are headed to a neutral market.

"New home construction is still needed to keep prices and housing supply healthy in the long run.” As new construction begins to be built, there will be increased downward pressure on the prices of existing homes on the market.

Takeaway: Supply is about to increase significantly. The supply of existing homes is already increasing and the number of newly constructed homes is about to increase.

“Rising inventory bodes well for slower price growth and greater affordability, but the amount of homes for sale is still modestly below a balanced market.” In real estate, there is a guideline that often applies. When there is less than 6 months inventory available, we are in a sellers’ market and we will see appreciation. Between 6-7 months is a neutral market where prices will increase at the rate of inflation. More than 7 months inventory means we are in a buyers’ market and should expect depreciation in home values. As Yun notes, we are currently in a sellers’ market (prices still increasing) but are headed to a neutral market.

"New home construction is still needed to keep prices and housing supply healthy in the long run.” As new construction begins to be built, there will be increased downward pressure on the prices of existing homes on the market.

Takeaway: Supply is about to increase significantly. The supply of existing homes is already increasing and the number of newly constructed homes is about to increase.

Monday, July 7, 2014

Rental Payment Histories May Count in Credit Scores

Daily Real Estate News

Renters who have never been late with a rent payment will find that their stellar record wont do anything to lift their credit scores when it comes time to shop for a mortgage. But that may soon change: Two of the main credit reporting agencies, Experian and TransUnion, reportedly are starting to incorporate verified rental payment data into credit files and using it to compute the consumers' credit scores when they apply for a mortgage. "At a time when record numbers of first-time buyers are missing in action in the home-purchase market — many of them in part because their credit scores don't make the grade — the non-reporting of key credit records is costly to them and the economy as a whole," The Columbus Dispatch reports. Some companies also are stepping in to ensure renters get their on-time payment histories included when applying for a mortgage. ECredable, an alternative credit data company, says it will verify renters' payment histories that haven't been reported to the major credit bureaus, and then generate a credit report and score. Potential home buyers are then urged to present the report to mortgage loan officers and ask that the information be considered in their application for a mortgage (which the lender is required to do under federal credit regulations).

Renters who have never been late with a rent payment will find that their stellar record wont do anything to lift their credit scores when it comes time to shop for a mortgage. But that may soon change: Two of the main credit reporting agencies, Experian and TransUnion, reportedly are starting to incorporate verified rental payment data into credit files and using it to compute the consumers' credit scores when they apply for a mortgage. "At a time when record numbers of first-time buyers are missing in action in the home-purchase market — many of them in part because their credit scores don't make the grade — the non-reporting of key credit records is costly to them and the economy as a whole," The Columbus Dispatch reports. Some companies also are stepping in to ensure renters get their on-time payment histories included when applying for a mortgage. ECredable, an alternative credit data company, says it will verify renters' payment histories that haven't been reported to the major credit bureaus, and then generate a credit report and score. Potential home buyers are then urged to present the report to mortgage loan officers and ask that the information be considered in their application for a mortgage (which the lender is required to do under federal credit regulations).

Friday, July 4, 2014

July 4th - Declaration of Independence

Variously known as the Fourth of July and Independence Day, July 4th has been a federal holiday in the United States since 1941, but the tradition of Independence Day celebrations goes back to the 18th century and the American Revolution (1775-83). In June 1776, representatives of the 13 colonies then fighting in the revolutionary struggle weighed a resolution that would declare their independence from Great Britain. On July 2nd, the Continental Congress voted in favor of independence, and two days later its delegates adopted the Declaration of Independence, a historic document drafted by Thomas Jefferson. From 1776 until the present day, July 4th has been celebrated as the birth of American independence, with typical festivities ranging from fireworks, parades and concerts to more casual family gatherings and barbecues.

HAPPY JULY 4 TO EVERYONE AND BE SAFE !!!

From: http://www.history.com/topics/holidays/july-4th

HAPPY JULY 4 TO EVERYONE AND BE SAFE !!!

From: http://www.history.com/topics/holidays/july-4th

Thursday, July 3, 2014

Housing Market Forecast

- The housing market is beginning to roar back. Existing home sales have risen for two straight months after suffering declines since the summer months of last year. The pending contracts also show robust gains, implying home sales will further rise over the near term. Also there is sizable pent-up housing demand looking to emerge. The timing is uncertain. But the pent-up demand implies home sales have much room to rise over the next few years.

- Existing home sales rose 4.9 percent in May from the prior month after accounting for normal seasonal factors. (Sales increased 12 percent on a raw count, but the bulk of that increase was due to the normal April to May seasonal upswing that occurs every year.) Now that pending home sales have increased by 6 percent in May, the closing activity is assured to rise further over the next two months.

- One key factor that had held back home sales late last year and early this year was simply lack of inventory. If there are too few homes for sale then only too few homes will get sold. Now inventories are rising, not only on a monthly basis, but also from the same time one year ago. This bodes very well for more consumers getting into the market. One has to also remember that the increase in inventory is not only in pure supply, but many families are putting their home on the market in order to buy their next desired home. That is, the increases in inventory are also a reflection of increases in demand for home buying.

- Newly constructed home sales also have been perking up. In May, new home sales surpassed the 500,000 annualized sales pace for the first time in 6 years. With the quickening pace of new home sales, homebuilders will want to create more dust and construct more new homes. That means more new home inventory on the way.

- When home prices were rising at double-digit rates of appreciation, potential homebuyers naturally paused to wonder: is it a new bubble? Or can I afford these prices? But price appreciation has greatly moderated and is rising at only a few percentage points above wage growth. Therefore, potential homebuyers will no longer face the sticker shock and can now make rational decisions about whether or not it makes sense to buy a home.

- There clearly appears to be large pent-up demand. Comparing current supporting factors for potential home sales with actual home sales show a mismatch. Back in the year 2000, a good reference year for comparison since there was neither bubble nor bust at that time, existing home sales reached over 5 million while new home sales nearly touched 1 million. Today, home sales activity is below that. However, there are 6.5 million additional jobs and 36 million additional people living in the country. Mortgage rates are also markedly lower today. Therefore, potential home sales are measurably larger than what we are observing. Home sales have plenty of room for a further rise.

- The outlook, therefore, is for housing starts and new home sales to rise comfortably this year and the next. Existing home sales, due to a sluggish first quarter, will fall a bit short in annual tally this year, but will show growth in 2015. Home prices will rise, though at a manageable single-digit rate of appreciation over the next two years.

Housing Market Forecast Posted in Economic Updates, Economist Commentaries, by Lawrence Yun, PhD., Chief Economist and Senior Vice President

Wednesday, July 2, 2014

Pending Home Sales Surge 6.1%

Pending home sales posted a sharp 6.1 percent rise in May, as lower mortgage rates and rising inventories helped propel the market into the summer season, according to the National Association of REALTORS®’ Pending Home Sales Index, a forward-looking indicator based on contract signings. It was the largest month-over-month gain on the index since April 2010, when first-time home buyers were rushing to sign purchase contracts before a popular tax credit program ended.

Guess what?

Existing-home sales are getting a lift, too. All four regions across the country posted increases in pending home sales in May, led by the Northeast and West.

“The flourishing stock market the last few years has propelled sales in the higher price brackets, while sales for homes under $250,000 are 10 percent behind last year’s pace,” says Lawrence Yun, NAR’s chief economist. “Meanwhile, apartment rents are expected to rise 8 percent cumulatively over the next two years because of tight availability. Solid income growth and a slight easing in underwriting standards are needed to encourage first-time buyer participation, especially as renting becomes less affordable.”

Yun says home sales will likely rise the second half of the year but “won’t be enough to compensate for the sluggish first quarter and will likely fall below last year’s total.” Despite the rise in May, pending home sales remained 5.2 percent below their levels a year ago.

By Region

The following is a breakdown by region of the latest Pending Home Sales Index reading: ·

Existing-home sales are getting a lift, too. All four regions across the country posted increases in pending home sales in May, led by the Northeast and West.

“The flourishing stock market the last few years has propelled sales in the higher price brackets, while sales for homes under $250,000 are 10 percent behind last year’s pace,” says Lawrence Yun, NAR’s chief economist. “Meanwhile, apartment rents are expected to rise 8 percent cumulatively over the next two years because of tight availability. Solid income growth and a slight easing in underwriting standards are needed to encourage first-time buyer participation, especially as renting becomes less affordable.”

Yun says home sales will likely rise the second half of the year but “won’t be enough to compensate for the sluggish first quarter and will likely fall below last year’s total.” Despite the rise in May, pending home sales remained 5.2 percent below their levels a year ago.

By Region

The following is a breakdown by region of the latest Pending Home Sales Index reading: ·

- Northeast: contracts rose 8.8 percent month-over-month in May and are 0.2 percent above year-ago levels.

- Midwest: contracts rose 6.3 percent month-over-month in May but remain 6.6 percent below May 2013 levels.

- South: contracts increased 4.4 percent month-over-month in May but are 2.9 percent below year-ago levels.

- West: contracts increased 7.6 percent month-over-month in May but remain 11.1 percent below May 2013 levels.

Tuesday, July 1, 2014

5 Tips to Save Energy During the Summer

Summer is here and Arizona heat is also here and will be here for another 4 months or so. Blasting the A/C may sound like a great plan but not for your energy use especially your wallet. A few adjustments of your energy use will make a difference on your home and budget.

First tip is to set the temperature 2 degrees higher when you are leaving your house. Gadgets like computers, coffee makers, and home entertainment centers still uses energy even when not in use. Unplug these gadgets to minimize energy drain.

During the summer months in the Valley, it’s impossible to not turn on your air conditioner. Maintenance of A/C by cleaning or replacing your air filters each month can also save energy. Keeping air ducts clean and unblocked will keep the system running smoothly and efficiently.

When washing clothes, 90% of energy used is to heat water. When washing clothes, switched from hot to warm or warm to cold. By doing this, you are saving drastically on use of energy.

Use a ceiling fan more. A ceiling fan does not really cool a place but it gives a breeze that makes you cooler and comfortable.

Get smart: All homes are not created equal. Energy-smart features, such

as low-E windows, solar-electric power options and high-performance

insulated stucco will help you achieve the energy-saving benefits you

desire.

Subscribe to:

Comments (Atom)